The rapid proliferation of drones, loitering munitions, and low-cost aerial threats is redefining modern conflict, driving armed forces worldwide to rethink how air defence, force protection, and battlefield sustainability are achieved. As threats continue to evolve, so too must the platforms, weapon systems, and sensors designed to counter them, with one clear objective: restoring operational and economic advantage against increasingly asymmetric and saturated attack environments.

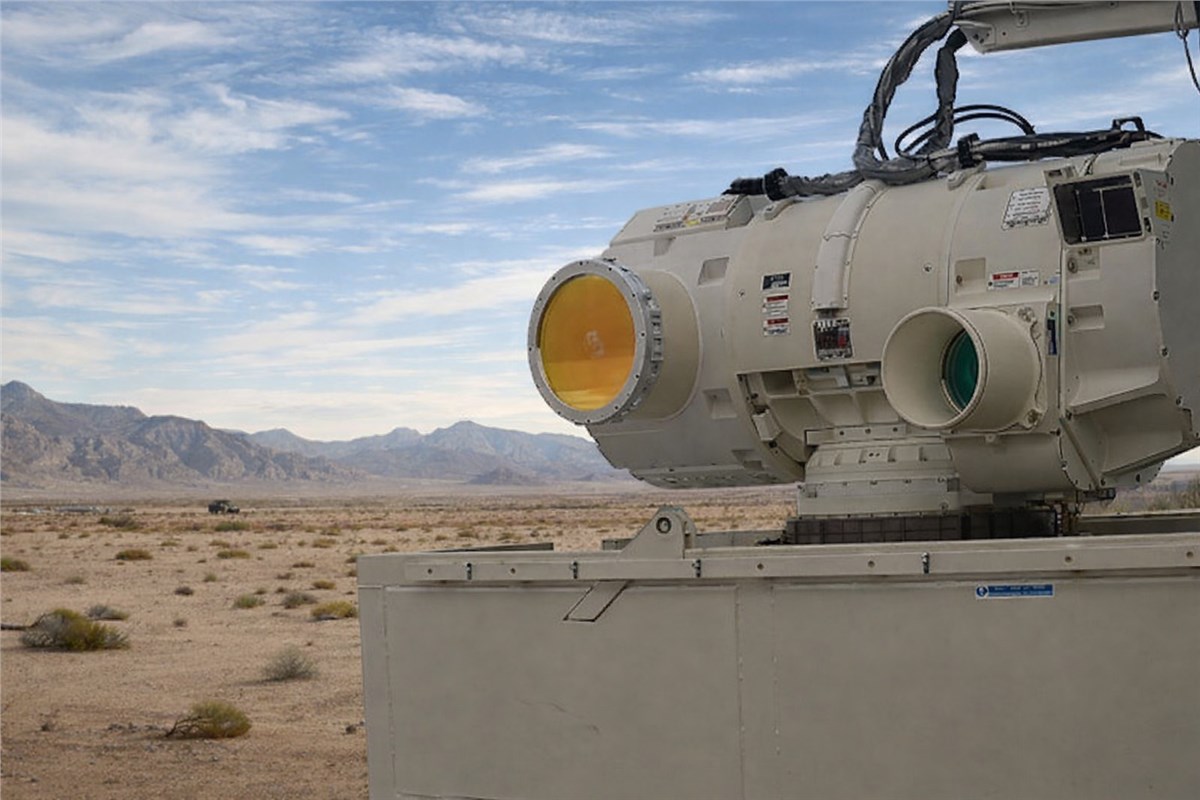

Against this backdrop, the operational fielding of directed energy weapon (DEW) systems such as the UK’s DragonFire and Israel’s Iron Beam, alongside parallel efforts in the United States, Europe, and Asia, marks a defining moment in the evolution of modern military capabilities. For the first time, DEWs are moving decisively beyond experimental programmes and limited trials into active service, signalling the emergence of a new class of weapons within global defence architectures.

Recent operational lessons from Ukraine, the Middle East, and other conflict zones have highlighted the limitations of relying solely on missile-based air defence to counter large volumes of low-cost threats. The widespread use of commercial drones, improvised aerial systems, and loitering munitions has demonstrated how adversaries can impose disproportionate costs on even the most advanced militaries. In response, defence establishments are accelerating the integration of high-energy lasers and high-power microwave systems into layered air defence architectures as a means to rebalance the cost-exchange equation.

Market forecast by Region, Domain, Type, Lifecycle phase, and Deployment. Country Analysis, Market and Technology Overview, Critical Raw Materials, Opportunity Analysis, and Leading Company Profiles

Download free sample pages More informationAs western forces pivot toward preparing for near-peer and peer-level competition, DEWs are emerging as a critical complement to traditional kinetic interceptors. Their ability to engage targets at the speed of light, with deep magazines constrained primarily by power availability rather than ammunition stockpiles, makes them particularly well-suited to countering massed and persistent aerial threats. This is driving renewed emphasis on multi-role air defence systems that integrate sensors, command-and-control, kinetic weapons, electronic warfare, and directed energy within a single operational framework.

The evolving threat environment, enriched by the widespread availability of commercial-off-the-shelf technologies and dual-use components, has further strengthened the case for non-kinetic defensive solutions. As a result, militaries are increasingly investing in vehicle-mounted and emplaced laser systems for counter-UAS missions, alongside high-power laser and microwave systems for short-range air defence and base protection. These investments are being guided not only by tactical requirements, but also by the imperative to maximise return on investment in an era of constrained defence budgets and rising operational tempo.

DragonFire and Iron Beam illustrate that long-standing technical barriers related to power scaling, beam control, and thermal management are now being overcome in real operational environments. Their deployment validates directed energy not merely as a niche capability, but as a practical and increasingly indispensable component of modern force structures.

From an industrial perspective, the DEW market differs fundamentally from traditional munitions markets. While production volumes are expected to remain lower than missile or artillery systems, the value density of DEWs is high, driven by advanced photonics, power electronics, thermal management, and software-defined fire control systems. The market is therefore characterised by strong opportunities in specialised manufacturing, system integration, and critical raw materials, rather than mass production alone.

The current strategic environment—shaped by sustained conflict in Eastern Europe, instability in the Middle East, and intensifying competition in the Indo-Pacific—is expected to provide a strong tailwind for DEW adoption. North America and Europe are likely to capture the largest share of near-term DEW investments, driven by active counter-UAS requirements, base defence modernisation, and NATO-aligned air defence upgrades, while Asia–Pacific is set to emerge as the fastest-growing region as regional powers accelerate indigenous DEW programmes.

As militaries seek to sustain high-tempo operations, manage escalating costs, and defend against increasingly diverse aerial threats, directed energy weapons are moving from experimental concepts to operational necessities—positioning the DEW market for a structural breakout over the coming decade and marking the opening chapter of a new era in modern warfare, where energy itself becomes a primary instrument of defence.

Arlington, VA

Jul 8 - 9, 2026